Whether or not to quarantine sick members or employees at the chapter house is up to each individual chapter and house corporation to decide based on their organization’s guidance, their campus and local health department guidance, and the structure and layout of their individual facilities.

Many of our clients are feverishly preparing for their members to return to campus, both resident and non-resident. We can only imagine the stress and anxiety that you are facing as you navigate the opening of your chapter house. We appreciate you and your leadership as you face this challenge, you need to be confident in knowing that your organization has secured a comprehensive insurance policy to cover the entities and your exposure to liability.

As we have urged, we are confident that you will implement the COVID-19 CDC guidelines, you will have trained your staff on the procedures, and you will have educated all your collegiate members on the safety guidelines. Having done so and doing your best to get compliance, your liability will be significantly reduced. The standard is “what a prudent and reasonable person would do.”

During these chaotic times, the comprehensive insurance coverage that your organization has purchased hopefully gives you the freedom to make the best business decisions for your chapter or house corporation.

Safety measures are being implemented for not only your collegiate members, but just as importantly, for your employees. We recently had a question that we wanted to address for reference. The question was what should be done if the house director becomes ill with the COVID-19 virus.

Below are some points to consider:

- If the house director has a private entrance and bath, it can be much easier to quarantine an individual in this space. If the chapter house is her only home, you can have her stay at the house. Safety measures must be considered during her quarantine time (see our Things to Consider Before Reopening resource for further guidance).

- If there is no private entrance and bath, your options become more limited and must be carefully considered.

- In quarantine, she will not be able to perform her usual duties, so a temporary employee will need to be hired that would not necessarily need to live in the chapter house who could assume these duties.

- Should you hire an additional employee, we would ask that you contact us to discuss any insurance implications which are doubtful. Workers’ compensation laws are very strict, and we don’t want you being at odds with these conditions.

- The insurance company does not require that the person who is doing the traditional house director functions live in the chapter house, so this gives you more options to consider.

- We would encourage you to look to your university as they may have graduate students or past RAs that could be used for this temporary period.

As always, please do not hesitate to contact your Client Executive should you have additional questions or need further guidance.

Campus dynamics dedicate how each chapter and house corporation adapts

As a house corporation volunteer, you are in the midst of reviewing the impact of the COVID-19 virus on the chapter operations and the possibility/probability of your college or university being opened this fall academic semester and what that would look like. We have come to understand that each and every campus will be deciding the best option for its students and that the sorority chapters will undoubtedly have to follow their lead.

Thus, we think that this is a good time to make a connection with the appropriate university personnel who can help you also navigate this matter more effectively. As a means of trying to establish a relationship/partnership with the university, we are suggesting some basic questions that you may want to consider asking to get a sense of where the university is currently thinking which may ultimately help you gauge your direction. As a private organization, you will have the choice to make the decisions that work best for your house corporation and the chapter but sharing information can also be of some assistance in this very challenging matter.

Click here for the continually updated list of University’s plans from The Chronicle of Higher Education.

Whom to contact at the university will vary by university, but we have seen many universities designated a COVID-19 taskforce. We recommend asking to speak to someone on the taskforce, if applicable. If that is not possible, the office of the Dean of Residential Life would be a great resource to connect with now, as well.

Consider determining the university’s position on the following:

- When will the decision be made by the university of their plans for the fall 2020 semester?

- Will you be encouraging your students to go home should they be tested positively for the COVID-19 virus?

- Will you provide quarantine/isolation rooms for all university students? Or just university housed students?

- Are you aware of any restrictions on a sorority to quarantine their members if they are in private fraternal housing?

- Have your faculty been advised on how to accommodate the needs of a quarantine student, such as online learning during their time of isolation?

- Will there be a specific cleaning service that the university is using that could also be used by the house corporations?

- Can we acquire cleaning solvents and supplies from the universities’ venders?

- Is there a chapter code of conduct in place currently from the university?

- Is there a university housing agreement in place that addresses the expectations of housing, should you choose to not close your chapter even though the university may be pushing all education online?

- Will the university be moving to house their students in single rooms from the typical two student room arrangements?

With the situation changing so frequently, please be sure you are reviewing the most updated version of this document and, as always, check with your national organization before taking any of these recommendations.

Whether or not to quarantine sick members at the chapter house is up to each individual chapter and house corporation to decide based on their organization’s guidance, their campus and local health department guidance, and the structure and layout of their individual facilities.

We have created some questions to consider in making the decision whether or not to quarantine sick individuals at the chapter house:

Exterior considerations

- Universities may have a quarantine area, but it may likely be only for university-housed students

- Campus health centers generally do not have overnight housing capabilities

- Transporting a known infected individual exposes more of the population to the virus should the student be forced to go home

- Students living in off-campus housing will likely self-quarantine

- Hospitals only have capacity for the most ill individuals, so a quarantine elsewhere will be required

Individual considerations

- The personal risk for serious illness from COVID-19 among the primary age-group of our student population is extremely low and those who do contract the illness are unlikely to need medical care

- Our member residents likely will not want to leave the chapter house and/or campus

Sorority considerations

- Does your housing agreement give you the permission to evict? Tenant laws are very liberal, so you may have trouble evicting a resident for non-compliance.

- It is difficult to isolate a person in many of our chapter facilities because of the recommendation for private rooms, bathrooms, etc.

- The delivery of food by employees poses an increased risk to our employees

- Does potential exposure to the virus by our employees bring on more workers’ compensation and employment practices liability exposure?

- How would volunteers coming on to your property feel about a known infected person on the property?

- If members know that they cannot stay at the house to be quarantines, are they more likely to be dishonest about their health?

- With no current immunity offered to businesses trying to re-open (though this is currently being proposed at the federal level), as you increase your duty of care, so too do you increase your potential liability.

- With enhanced education of best practices and close adherence to it, the isolation can be a low risk. The importance of education of your members remains one of the most critical parts of re-opening a chapter house and maintaining its operation.

- Creative solutions being explored will be necessary to be able to react quickly should a member become ill with the virus. Some examples we have heard mentioned:

- All campus house corporations jointly renting a four-bedroom apartment to serve as a quarantine site

- All members should be urged to have a “crash bag” that can be grabbed if they take ill or they have to move because a roommate becomes ill.

RELATED FAQ: WHAT LEGAL LIABILITY DOES A CHAPTER/HOUSE CORPORATION HAVE IF A MEMBER IS DIAGNOSED WITH THE COVID-19 VIRUS AND IS ALLOWED TO LIVE IN THE CHAPTER HOUSE UNDER A QUARANTINE OR ISOLATION ROOM?

Legal liability exists when:

- The wrongdoer (chapter house or corporation) is found guilty of “negligent conduct” meaning they breached a duty owed to the injured party

- The injured party suffers actual damages such as getting ill with the virus

- The wrongdoer’s negligent conduct is the proximate cause of the injury or damage

What actions during the COVID-19 crisis could possibly lead to the insured (chapter and/or house corporation) being found legally liable for an injury from the virus? Before we lay out some examples it is always important to remember that society and the courts generally only require that a person or entity act “as a reasonable and prudent person” and using their best, and most informed, judgement act accordingly.

Examples might be:

- Allowing an employee who is known to be infected with the virus to continue working

- Forcing an employee to continue to work in a chapter house where there are resident members who are ill and isolated at the house

- Failure to adhere to required health and prevention guidelines

- No efforts to educate your employees and/or members on the health and prevention guidelines

- Remaining open following an order by a civil authority to close

- Indiscriminate application of rules and guidelines for the members of how to safely live in the chapter house to not expose your sisters to the virus

There are numerous other scenarios; however, the major point is that there will be advice from experts like the CDC on how to follow health and prevention guidelines to keep your chapter house safe from spreading COVID-19. The key is to follow the health and prevention guidelines, educate your employees and members on these guidelines, and put measures in place to ensure their compliance of these guidelines. Should someone get injured or ill and allege they did so on your property, you will be able to confidently defend your position by having followed these best practices.

This letter was created for clients to proactively answer frequently asked insurance questions for parents and members before the questions arise throughout the course of a member’s collegiate experience.

Please feel free to use this template and edit it as you see fit. You will notice [bracketed] sections where we encourage you to insert your organization and/or chapter name to tailor this language to your specific needs.

Should you have any questions, as always, please do not hesitate to contact us.

Re: [Fraternity’s] National Insurance Program

To The Parents of [Chapter Member’s Name]:

The Independent Insurance Agents of America estimate that 100,000 property claims occur on college campuses annually. While on a college campus, your young adult will be responsible for the personal property or personal possessions they have at school. They also are liable for their actions that cause damage to others’ property and/or any bodily injury they cause to another person.

If your family has a standard homeowner’s insurance policy or a renter’s insurance policy, it is likely that the exposures to your young adult will be covered under that policy while they are away at college. However, we recommend that chapter members and their families verify that their homeowners policy extend to a student’s personal property while away at college.

For that reason, we believe that it is our responsibility to communicate to the chapter members and their parents the specifics of the Sorority’s insurance coverage.

Property and Liability Coverage

Each House Corporation has a contract with the resident members that defines the relationship and obligation of both parties to the arrangement. The agreement explicitly states that the House Corporation is not responsible for any loss or damage to a resident member’s personal property, including their personal automobiles. Personal property includes members’ laptops, personal items, and any other property that they bring into the chapter house. Similarly to any other rental arrangement, the resident is responsible for insuring their own personal property, either via their parent’s homeowners policy or via a renters’ policy. The fraternity’s property coverage covers the Fraternity’s property, for example the furniture and kitchen equipment owned by the Housing Corporation at the chapter house.

Parents’ Homeowner’s Policy

It is the responsibility of the resident member to make sure that their personal property is protected while living in the chapter house. Many chapter members’ property would still be covered under their parent’s homeowners policy; however, we recommend that chapter members and their families verify that their homeowners policy extends to a student’s personal property while away at college.

We have reviewed the industry-standard insurance language for homeowner’s policies in hopes of providing resident members with the information necessary to ensure that their personal property is adequately protected. The standard homeowner’s policy language defines an insured as:

- A student in school full time, as defined by the school, who was a resident of your household before moving out to attend school, provided the student is under the age of:

- 24 and your relative; or

- 21 and in your care or the care of a person described above (there have been a number of states that have enacted legislation that extends the age limit beyond 21 years, so be sure to verify the age limit in your insurance policy language)

Most resident members would fit into one or both of the definitions above, but there are further issues to consider when ensuring your personal property is protected:

- College students are typically covered for ten percent of the contents limit under their parent’s homeowner’s policy. If your personal property is valued at or above the ten percent limit under your policy, you should speak with your insurance agent about increasing that limit.

- Under the standard homeowner’s policy, the contents coverage only provides named perils coverage, which means that losses would be covered only if they arise from causes of loss listed in the policy. A laptop that was damaged from power surge or from being dropped, for example, would likely not be covered under a named perils policy. We recommend that you verify with your insurance agent that the policy provides all-risk coverage.

- If a student chooses to declare independent status, perhaps for loan purposes, they would likely not be covered under their parent’s homeowner’s policy.

Student Renter’s Insurance

If you would prefer not to rely on a parent’s renter’s or homeowner’s insurance, we highly encourage you or your daughter to purchase student renter’s insurance, which will cover her personal property and personal liability. For example, National Student Services offers $10,000 worth of coverage with a $50 deductible for about $300 in annual premium. Grad Guard offers a comparable program. If you or your daughter purchases a student renter’s policy, we recommend that you confirm that the following perils are covered: theft, fire, flood, and wind. In addition, some of the most common causes of loss to a laptop include drops and damage from liquids being spilled into the laptop, so it is important to verify whether or not those types of claims would be covered.

Personal Liability Coverage

The organization’s liability insurance does not cover personal or bodily injury to your daughter in much the same way that your homeowner’s policy does not provide medical coverage for members of your household. If your daughter is injured at the chapter house or at a chapter event, she will need to rely on her (or your) personal medical policy. This may also be spelled out in the membership and housing agreements that she has signed.

[Sorority name’s] policy will provide liability coverage for your daughter’s personal actions within the course and scope of her membership obligations, but not outside. Your daughter’s organization has purchased the broadest coverage possible to protect your daughter should she be named in a lawsuit due to her affiliation with [sorority name], so long as she is following the guidelines of the organization. The liability insurance is third-party coverage, meaning that it protects the insureds (the Sorority, House Corporation, Chapter, Members, Volunteers, etc.) should they be named in a lawsuit from a third-party who has either been hurt or had their property damaged.

Personal Automobile Insurance

If your daughter takes her car to school, your automobile policy will continue to cover her personal automobile while she is away at school. If she does not take a car with her to school, you will want to ensure that she is still listed as a driver under your automobile policy if she plans to drive any automobile while away at school. Several insurance companies offer “student away at school” discounts for this type of coverage, so be sure to check with your insurance agent before she leaves for college. MJ recommends that drivers, for their own financial health, carry at least $300,000 of automobile coverage, not merely the minimum coverage required by your state.

If your daughter drives her personal automobile on Sorority business and is involved in an accident, she will not be covered by [sorority’s name] automobile liability policy. Liability follows the owner of the car; thus her personal liability would be covered by her personal automobile policy. The organization’s automobile liability policy exists to protect the organization if it is named in a lawsuit involving an automobile, not individuals. For more information about the automobile coverage, please refer to the Digging Deeper: Non-Owned Automobile document on MJ’s website.

For many chapter members, college is the first opportunity for them to live on their own away from home. It is important that chapter members and their families take the necessary steps to ensure that their personal property, which can often be very expensive, is financially protected via insurance. If you are interested in studying the organization’s insurance program further, we recommend you review the expansive Insurance Summary on MJ’s website. We realize that this can be a confusing issue, so please do not hesitate to contact us with any questions or concerns.

Officer Liability

There is no debate that all students on campus will be expected to continue to follow the rules that universities and fraternal organizations put in place to ensure the health and safety of the students, faculty, and community.

It also goes without saying that the sorority officers of the chapter will have more responsibility to help lead this effort. With increased responsibilities comes greater liability to act as a “reasonable and prudent person” would do in a similar situation. If your daughter is a chapter officer, she has been and continues to be covered under the [Sorority’s] national insurance policy. We remain confident that your daughter would see her organization’s policy step up to defend her should she be named in a lawsuit and pay for a judgement should she be found negligible in her duties as an officer. You can be confident in the comprehensive national insurance policy that your daughter’s organization has secured for their exposures to risk.

Sincerely,

Kit Clark Moorman

Director of Risk Management Education

MJ Sorority

Other helpful resources:

- Insurance Basics for Member’s Parents Webinar: We have created a self-guided presentation that explains how the organization’s insurance program works, as well as provides some helpful hints regarding homeowners or renter’s insurance coverage.

- Insurance and Risk Management Summary: An expansive explanation of the organization’s insurance program in straightforward and accessible language.

- www.mjsorority.com: A one-stop resource for all things related to risk management and insurance issues from the leader in women’s fraternity and sorority risk management needs.

With the situation changing so frequently, please be sure you are reviewing the most updated version of this document and, as always, check with your national organization before taking any of these recommendations.

As we navigate these crazy times dealing with the COVID-19 pandemic, we are trying to address as many possible scenarios that need to be addressed for chapter facilities to safely open and stay open. We are relying on the experts and doing our best to collect the experts’ advice and information that impacts our clients. It is important that our clients are staying as up-to-date as possible on the current recommendations by their respective national organization, by their state and local governments, and by the campus (including campus health and residential life departments) in which they are affiliated.

The following guidance was created to help advise house corporations and chapters – working together with residents, employees, and public health officials – prevent the spread of COVID-19. As information is rapidly changing and evolving, please ensure you are following the advice of your national organization and local public health guidance.

Challenges specific to sorority chapter houses

We have been researching various scenarios and questions that face sororities specifically. Because each chapter facility faces unique challenges depending on their specific facility, their campus, state, etc., we cannot offer clear guidance that applies to every chapter house. For that reason, we are offering the advice on the following situations with the stipulation that each location will need to do what is best for their individual situations, ensuring that they are following their own organization’s policies and the guidance from local and campus public health departments.

Cold dorms/warm dorms/sleeping porches/other group sleeping arrangements

The risks associated with the communal sleeping arrangements that do exist in some sorority chapter houses will need to be closely reviewed. At face value, these congested/densely populated and poorly ventilated rooms will be a breeding ground for the virus and the eventual spread to others in the same room. If it is possible to utilize the personal rooms for the temporary sleeping arrangements, this would be the best recommendation; however, we recognize that this may not be possible from a business perspective. This is another example of where you must chose your risks, so to speak, and the business risk to your operation with significantly less members paying room and board may outweigh the risks of members being exposed to the virus.

Some best practices to consider should you have no choice but to maintain the usual group sleeping arrangements are as follows:

- To the extent that physical barriers can be used to segregate the sleeping beds, this will possibly minimize, but not eliminate the risk of the virus spreading.

- We also believe that an increase in the flow of air throughout the room and a neutralizer such as an air filtering system should also be considered.

- The cleaning of these rooms will have to be significantly enhanced in order to remove any virus from the hard surfaces of the room and the cleaning of the soft surfaces should also be given more attention by the members (see CDC guidelines).

- helpful resource.

Importance of communication

Communication during a crisis is crucial, and it is possibly even more important during a global pandemic, in which conditions are changing sometimes multiple times during the same day. It has become abundantly clear that the success of a university and a sorority chapter house to be able to maintain operations will be closely tied to the students’ and members’ commitment to follow the best practices established. It is of utmost importance that communication lines are open between the chapter and House Corporation leadership and the following entities:

- University officials

- It is important that someone from the House Corporation and/or chapter is communicating with the University health department and residential housing personnel to stay updated with what steps the University is considering in order to stay open.

- Here is a resource we have created that offers some questions that we recommend you discuss with your university contact(s).

- state and local health departments

- Your national organization. Your sorority Headquarters will be making decisions and offering guidance. It is imperative that you stay in touch with them regarding re-opening specifics.

- Parents and members. It is imperative that clear and frequent communication is open between the House Corporation/Chapter and the members and their parents. We have modified our Letter to Member’s Parents resource to include some verbiage regarding COVID-19. We also created some sample verbiage for an addendum to the membership agreement that you are welcome to use and/or modify for your purposes.

Importance of House Corporation Board and Chapter Advisory Boards communication

- During normal times, it is important to clearly delineate House Corporation business from chapter business; however, these are extraordinary times, and it is important that the House Corporation and Chapter Advisor(s) are in open and continual communication with each other in order to share information regarding possible re-opening and what steps will be necessary to re-open the chapter house.

- We recommend that the House Corporation and chapter be on the same page regarding communication with members and their parents to ensure that expectations to live in the chapter house during the COVID-19 pandemic are accepted by the members and their parents. Our sample verbiage for the Member Agreement addendum can be found here.

- One of the biggest concerns of the sorority leadership is the support of the collegiate and alumnae members to follow the operating guidelines for each campus. It will be critical that the members know the rules and guidelines and that there will be strict reinforcement of these rules and guidelines. Being aware of the division of responsibility between the house corporations and chapter advisors, it will be critical that the standards boards are aware of the important role that they will plan in keeping the sorority houses in operation.

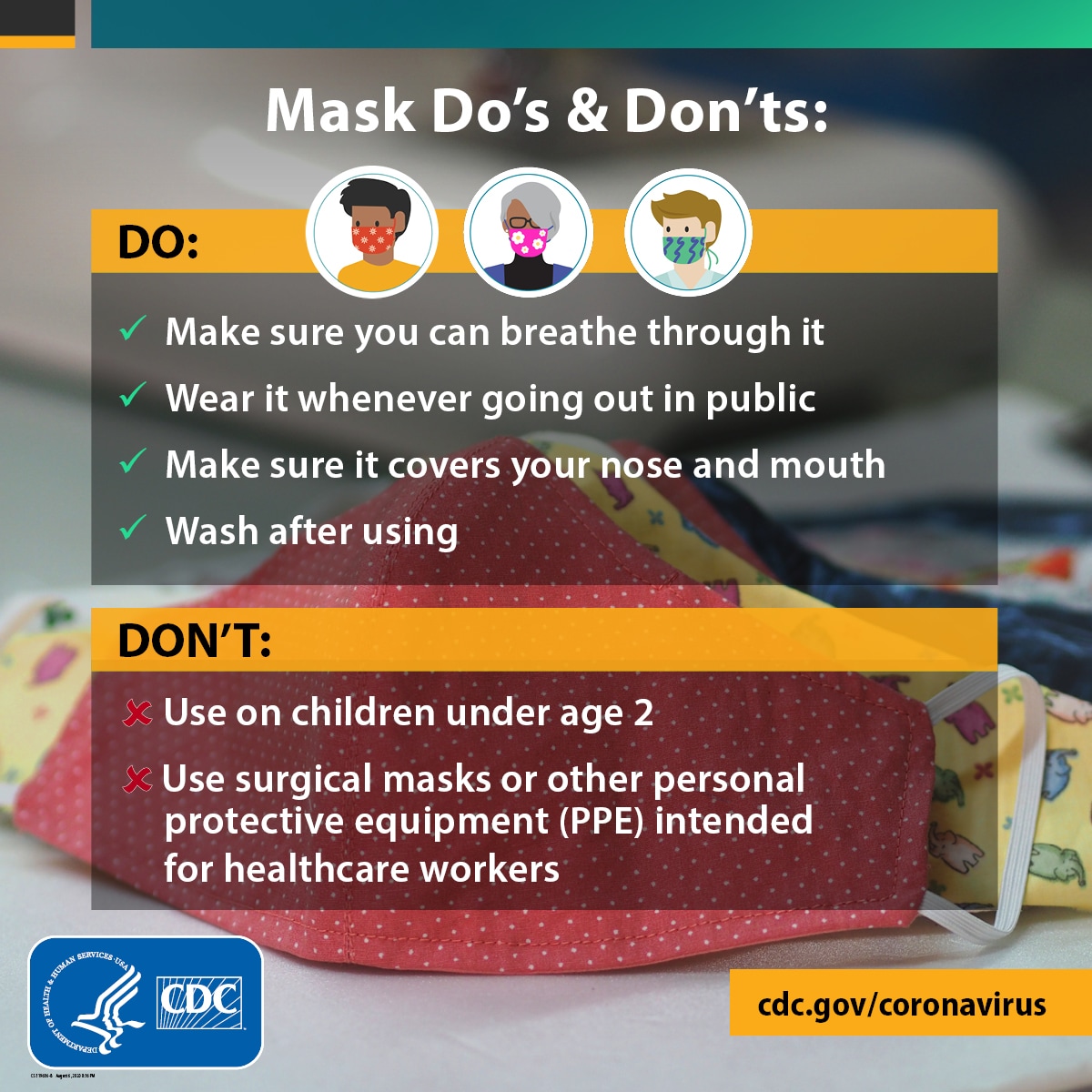

- Post signs in highly visible locations (e.g., building entrances, restrooms, dining areas) that promote everyday protective measures and describe how to stop the spread of germs (such as by properly washing hands and properly wearing a mask).

- Include messages (for example, these videos and resources from the National Panhellenic Council) about behaviors that prevent spread of COVID-19 when communicating with members and employees.

{kind=link}

Quarantining sick members

Whether or not to quarantine sick members at the chapter house is up to each individual chapter and house corporation to decide based on their organization’s guidance, their campus and local health department guidance, and the structure and layout of their individual facilities.

We have created some questions to consider in making the decision whether or not to quarantine sick members at the chapter house.

If a location does choose to quarantine ill members, this is the CDC guidance for quarantining sick members. Kappa Alpha Theta created this housing and safety plan that they graciously agreed to share, which includes a simple approach and expectations should a member be symptomatic or test positive. Each sorority is using a slightly different philosophy, but many general principles are mutual.

Quarantining a House Director

Generally, a house director has a private living arrangement that would lend itself to a quarantine. However, this does not align well with the house director being able to continue to perform their job responsibilities. A possible alternative may be to secure a temporary employee to temporarily takeover the house director’s responsibilities for oversight of the property.

See our resource on additional things to consider if your House Director tests positive for COVID-19.

Social distancing challenges

The CDC guidance on social distancing is particularly difficult in communal living spaces. We recommend the following measures be put in place should you chose to re-open the chapter house:

- Move all chapter meetings to virtual meetings.

- The CDC recommends the following in terms of shared meal times/spaces:

- Arrange seating of chairs and tables to be least 6 feet apart during shared meals or other events.

- Alter schedules to reduce mixing and close contact, such as staggering meal and activity times and forming small groups that regularly participate at the same times and do not mix.

- If your facility has group sleeping arrangements, try to create more space and ventilation in those areas to maintain adequate social distancing. In general sleeping areas (for those who are not experiencing respiratory symptoms), try to make sure resident’s faces are at least 6 feet apart and align sleeping arrangements/beds so residents sleep head-to-toe.

- All staff and resident members should wear a cloth face covering when in shared areas of the facility and maintain social distancing to slow the spread of the virus.

- Limit all visitors to the facility, including volunteers.

- Again, the house corporation and the chapter need to be in close communication to carefully consider how to accommodate non-resident sorority members and their access to the sorority house.

Additionally, the CDC recommends the following considerations for common spaces in your facility.

Higher-risk individuals

We recommend that our clients offer tremendous flexibility to employees and members at higher risk of infection. Based on what we currently know, the CDC defines those individuals at higher risk of severe illness from COVID-19 as follows:

- People 65 years and older

- People of all ages with underlying medical conditions, particularly if not well controlled, including:

- People with chronic lung disease or moderate to severe asthma

- People who have serious heart conditions

- People with severe obesity (body mass index [BMI] of 40 or higher)

- People with diabetes

- People with chronic kidney disease undergoing dialysis

- People with liver disease

- People who are immunocompromised

- Many conditions can cause a person to be immunocompromised, including cancer treatment, smoking, bone marrow or organ transplantation, immune deficiencies, poorly controlled HIV or AIDS, and prolonged use of corticosteroids and other immune weakening medications

Employee considerations

It is important that employers are following the CDC guidance for businesses and employers. We recommend that all chapter house employees be provided with cloth face coverings and disposable gloves. When cleaning and disinfecting, employees should always wear gloves and gowns appropriate for the chemicals being used. Additional personal protective equipment (PPE) may be needed based on setting and product.

Here are some additional resources for review:

Testing

In order to re-open, it may be recommended to take temperatures of residents, employees, and guests. The federal government has waived certain HIPAA privacy rules during this emergency situation, but, again, it is important that you abide by the recommendations set forth by your national organization, your campus health department, and your state and local health departments for clarification.

Monitoring

It is important that you encourage member residents to monitor themselves for symptoms daily.

Disinfection and cleaning guidelines

The most important and relevant resource for decontamination is the CDC’s Guidance on Cleaning and Disinfection for Community Facilities. Stay tuned to the CDC guidance for the most updated information based on our evolving knowledge of the novel coronavirus. Review our recorded webinar on cleaning and decontamination recommendations.

Ventilation concerns

The Center for Disease Control (CDC) has recommended increased ventilation for COVID-19 prevention.

The CDC has stated that COVID-19 is spread mainly from person-to-person, through respiratory droplets produced when an infected person coughs or sneezes. The droplets can possibly be inhaled by people nearby. Because of this, the CDC recommends increasing building ventilation to cut down on recycled contaminated air.

Now, more than ever, it is imperative that HVAC system filters are inspected, exhaust systems are operational, and outside air sources are maximized. Many older buildings do not meet current codes, often lacking outside air intakes and exhaust. Even newer buildings, which may be equipped with intakes and exhaust, can be out of service or improperly balanced.

We urge you to consider this inspection as a part of your enhanced cleaning/decontamination work in your chapter house.

CDC guidance for communal living spaces

People living and working in sorority chapter houses will have challenges with social distancing to prevent the spread of COVID-19. In this type of shared housing, residents often gather together closely for social, leisure, and recreational activities, shared dining, and/or use of shared equipment, such as kitchen appliances, laundry facilities, stairwells, and elevators.

It is imperative that local house corporation and chapter volunteers are working together, communicating openly and often, and touching base with their state, local, and campus health departments, which can help you decide when and if you need to scale up or loosen prevention measures.

To maintain safe operations according to the CDC:

- Review the CDC guidance for businesses and employers to identify strategies to maintain operations and a healthy working and living environment.

- Develop flexible sick leave policies. Require staff to stay home when sick, even without documentation from doctors. Use flexibility, when possible, to allow staff to stay home to care for sick family or household members or to care for children in the event of school or childcare dismissals. Make sure that employees are aware of and understand these policies.

- Create plans to protect the staff and residents from spread of COVID-19 and help them put in place personal preventive measures.

- Clean and disinfect shared areas (such as exercise room, laundry facilities, shared bathrooms, and elevators) and frequently touched surfaces using EPA-registered disinfectants more than once a day if possible.

- Identify services and activities (such as meal programs, social activities, and exercise rooms) that might need to be limited or temporarily discontinued. Consider alternative solutions.

- Identify a list of healthcare facilities and alternative care sites where residents with COVID-19 can receive appropriate care, if needed.

Encourage staff and residents to prepare and take action to protect themselves and others

- Encourage social distancing by asking staff and residents to stay at least 6 feet apart from others and wear cloth face coverings in any shared spaces, including spaces restricted to staff only.

- Consider any special needs or accommodations for those who need to take extra precautions, such as older adults, people with disabilities, and people of any age who have serious underlying medical conditions.

- Limit staff entering residents’ rooms or living quarters unless it is necessary. Use virtual communications and check ins (phone or video chat), as appropriate.

- Limit the presence of non-essential volunteers and visitors in shared areas, when possible.

- Use physical barriers, such as sneeze guards, or extra tables or chairs, to protect front desk/check-in staff who will have interactions with residents.

- Provide COVID-19 prevention supplies for staff and residents in common areas at your facility, such as soap, alcohol-based hand sanitizers that contain at least 60% alcohol, tissues, trash baskets, and, if possible, cloth face coverings that are washed or discarded after each use.

- Consider any special communications and assistance needs of your staff and residents, including persons with disabilities.

- Suggest that residents keep up-to-date lists of medical conditions and medications, and periodically check to ensure they have a sufficient supply of their prescription and over-the-counter medications.

- If possible, help residents understand they can contact their healthcare provider to ask about getting extra necessary medications to have on hand for a longer period of time, or to consider using a mail-order option for medications.

- Make sure that residents are aware of serious symptoms of their underlying conditions and of COVID-19 symptoms that require emergency care, and that they know who to ask for help and call 911.

Note: Surgical masks and N-95 respirators are critical supplies that must continue to be reserved for healthcare workers and other medical first responders, as recommended by current CDC guidance. All staff and residents should wear a cloth face covering when in shared areas of the facility and maintain social distancing to slow the spread of the virus.

Communicate to staff and residents

Identify platforms such as email, websites, hotlines, automated text messaging, newsletters, and flyers to help communicate information on:

- Guidance and directives from state and local officials and state and local health departments.

- How your facility is helping to prevent the spread of COVID-19.

- How additional information will be shared, and where to direct questions.

- How to stay healthy, including videos, fact sheets, and posters with information on COVID-19 symptoms and how to stop the spread of germs, how to wash your hands, and what to do if you are sick.

- How staff and residents can cope and manage stress and protect others from stigma and discrimination.

- Identify and address potential language, cultural, and disability barriers associated with communicating COVID-19 information. Communications may need to be framed or adapted so they are culturally appropriate for your audience and easy to understand. For example, there are resources on the CDC website that are in many languages.

Considerations for common spaces in your facility, to prevent the spread of COVID-19

- Consider how you can use multiple strategies to maintain social (physical) distance between everyone in common spaces of the facility.

- Consider cancelling all public or non-essential group activities and events.

- Offer alternative methods for activities and social interaction such as participation by phone, online, or through recorded sessions.

- Arrange seating of chairs and tables to be least 6 feet apart during shared meals or other events.

- Alter schedules to reduce mixing and close contact, such as staggering meal and activity times and forming small groups that regularly participate at the same times and do not mix.

- Minimize traffic in enclosed spaces, such as elevators and stairwells. Consider limiting the number of individuals in an elevator at one time and designating one directional stairwells, if possible.

- Ensure that social distancing can be maintained in shared rooms, such as television, game, or exercise rooms.

- Make sure that shared rooms in the facility have good air flow from an air conditioner or an opened window.

- Consider working with building maintenance staff to determine if the building ventilation system can be modified to increase ventilation rates or the percentage of outdoor air that circulates into the system.

- Clean and disinfect shared areas (laundry facilities, elevators, shared kitchens, exercise rooms, dining rooms) and frequently touched surfaces using EPA-registered disinfectants more than once a day if possible.

Considerations for specific communal rooms in your facility

Shared kitchens and dining rooms

- Restrict the number of people allowed in the kitchen and dining room at one time so that everyone can stay at least 6 feet apart from one another.

- People who are sick, their roommates, and those who have higher risk of severe illness from COVID-19 should eat or be fed in their room, if possible.

- Do not share dishes, drinking glasses, cups, or eating utensils. Non-disposable food service items used should be handled with gloves and washed with dish soap and hot water or in a dishwasher. Wash hands after handling used food service items.

- Use gloves when removing garbage bags and handling and disposing of trash. Wash hands

Laundry rooms

- Maintain access and adequate supplies to laundry facilities to help prevent spread of COVID-19.

- Restrict the number of people allowed in laundry rooms at one time to ensure everyone can stay at least 6 feet apart.

- Provide disposable gloves, soap for washing hands, and household cleaners and EPA-registered disinfectants for residents and staff to clean and disinfect buttons, knobs, and handles of laundry machines, laundry baskets, and shared laundry items.

- Post guidelines for doing laundry such as washing instructions and handling of dirty laundry.

Recreational areas such as activity rooms and exercise rooms

- Consider closing activity rooms or restricting the number of people allowed in at one time to ensure everyone can stay at least 6 feet apart.

- Consider closing exercise rooms.

- Activities and sports (e.g., ping pong, basketball, chess) that require close contact are not recommended.

Shared bathrooms

- Shared bathrooms should be cleaned regularly using EPA-registered disinfectants, at least twice per day (e.g., in the morning and evening or after times of heavy use).

- Make sure bathrooms are continuously stocked with soap and paper towels or automated hand dryers. Hand sanitizer could also be made available.

- Make sure trash cans are emptied regularly.

- Provide information on how to wash hands properly. Hang signs in bathrooms.

- Residents should be instructed that sinks could be an infection source and should avoid placing toothbrushes directly on counter surfaces. Totes could also be used for personal items to limit their contact with other surfaces in the bathroom.

If a resident in your facility has COVID-19 (suspected or confirmed)

- Have the resident seek advice by telephone from a healthcare provider to determine whether medical evaluation is needed.

- If a resident has confirmed COVID-19, immediately notify the local health department and campus health department and communicate with staff and residents about potential exposure. Maintain confidentiality as required by the Americans with Disabilities Act (ADA) and, if applicable, the Health Insurance Portability and Accountability Act (HIPAA), and include messages to counter potential stigma and discrimination.

- Provide the ill person with information on how to care for themselves and when to seek medical attention.

- Encourage residents with COVID-19 symptoms and their roommates and close contacts to self-isolate – limit their use of shared spaces as much as possible.

- If possible, designate a separate bathroom for residents with COVID-19 symptoms.

- Consider reducing cleaning frequency in bedrooms and bathrooms dedicated to persons with COVID-19 symptoms to as-needed cleaning (e.g., soiled items and surfaces) to avoid unnecessary contact with the ill persons.

- Follow guidance on when to stop isolation.

- Minimize the number of staff members who have face-to-face interactions with residents who have suspected or confirmed COVID-19.

- Encourage staff, other residents, caregivers such as outreach workers, and others who visit persons with COVID-19 symptoms to follow recommended precautions to prevent the spread.

- Staff at higher risk of severe illness from COVID-19 should not have close contact with residents who have suspected or confirmed COVID-19, if possible.

- Those who have been in close contact (i.e., less than 6 feet with a resident who has confirmed or suspected COVID-19 should monitor their health and call their healthcare provider if they develop symptoms suggestive of COVID-19.

- Be prepared for the potential need to transport persons with suspected or confirmed COVID-19 for testing or non-urgent medical care. Avoid using public transportation, ride-sharing, or taxis. Follow guidelines for cleaning and disinfecting any transport vehicles.

Accepting guests at facilities

First, review and follow the guidance and directives from your state and local officials. It is our recommendation that chapter houses do not allow guests during the pandemic.

If you decide to allow guests, we recommend that you put in place check-in requirements and provide any guests with a clean cloth face covering.

With the situation changing so frequently, please be sure you are reviewing the most updated version of this document and, as always, check with your national organization before taking action.

The CDC has issued the following guidelines to properly disinfect your facilities before welcoming members, employees, and guests back in to the chapter facility.

Timing of cleaning

- Follow Interim Guidance for US Institutions of Higher Education on working with state and local health officials to isolate ill persons and provide temporary housing as needed.

- Close off areas visited by any ill persons. Open outside doors and windows and use ventilating fans to increase air circulation in the area. Wait 24 hours or as long as practical before beginning cleaning and disinfection.

- It is up to each individual chapter to decide whether or not to quarantine ill individuals. In areas where ill persons have been, follow Interim Guidance for Environmental Cleaning and Disinfection for U.S. Households with Suspected or Confirmed Coronavirus Disease 2019. This includes focusing on cleaning and disinfecting common areas where staff/others providing services may come into contact with ill persons.

- In areas where ill persons have visited or used, continue routine cleaning and disinfection as in this guidance.

- If it has been more than 7 days since the person with suspected/confirmed COVID-19 visited or used the facility, additional cleaning and disinfection is not necessary.

How to Clean and Disinfect

Hard (Non-porous) Surfaces

- If surfaces are dirty, they should be cleaned using a detergent or soap and water prior to disinfection.

- For disinfection, most common EPA-registered household disinfectants should be effective.

- A list of products that are EPA-approved for use against the virus that causes COVID-19 is available here. Follow the manufacturer’s instructions for all cleaning and disinfection products for concentration, application method and contact time, etc.

- Additionally, diluted household bleach solutions (at least 1000ppm sodium hypochlorite) can be used if appropriate for the surface. Follow manufacturer’s instructions for application, ensuring a contact time of at least 1 minute, and allowing proper ventilation during and after application. Check to ensure the product is not past its expiration date. Never mix household bleach with ammonia or any other cleanser. Unexpired household bleach will be effective against coronaviruses when properly diluted.

- Prepare a bleach solution by mixing:

- 5 tablespoons (1/3 cup) bleach per gallon of water or

- 4 teaspoons bleach per quart of water

- Prepare a bleach solution by mixing:

Soft (Porous) Surfaces

- For soft (porous) surfaces such as carpeted floor, rugs, and drapes, remove visible contamination if present and clean with appropriate cleaners indicated for use on these surfaces. After cleaning:

- If the items can be laundered, launder items in accordance with the manufacturer’s instructions using the warmest appropriate water setting for the items and then dry items completely.

- Otherwise, use products that are EPA-approved for use against the virus that causes COVID-19 and that are suitable for porous surfaces

- If the items can be laundered, launder items in accordance with the manufacturer’s instructions using the warmest appropriate water setting for the items and then dry items completely.

Electronics

- For electronics such as tablets, touch screens, keyboards, remote controls, and ATM machines, remove visible contamination if present.

- Follow the manufacturer’s instructions for all cleaning and disinfection products.

- Consider use of wipeable covers for electronics.

- If no manufacturer guidance is available, consider the use of alcohol-based wipes or sprays containing at least 70% alcohol to disinfect touch screens. Dry surfaces thoroughly to avoid pooling of liquids.

Linens, Clothing, and Other Items That Go in the Laundry

- In order to minimize the possibility of dispersing virus through the air, do not shake dirty laundry.

- Wash items as appropriate in accordance with the manufacturer’s instructions. If possible, launder items using the warmest appropriate water setting for the items and dry items completely. Dirty laundry that has been in contact with an ill person can be washed with other people’s items.

- Clean and disinfect hampers or other carts for transporting laundry according to guidance above for hard or soft surfaces.

Personal Protective Equipment (PPE) and Hand Hygiene:

- The risk of exposure to cleaning staff is inherently low. Cleaning staff should wear disposable gloves and gowns for all tasks in the cleaning process, including handling trash.

- Gloves and gowns should be compatible with the disinfectant products being used.

- Additional PPE might be required based on the cleaning/disinfectant products being used and whether there is a risk of splash.

- Gloves and gowns should be removed carefully to avoid contamination of the wearer and the surrounding area. Be sure to clean hands after removing gloves.

- If gowns are not available, coveralls, aprons or work uniforms can be worn during cleaning and disinfecting. Reuseable (washable) clothing should be laundered afterwards. Clean hands after handling dirty laundry.

- Gloves should be removed after cleaning a room or area occupied by ill persons. Clean hands immediately after gloves are removed.

- Cleaning staff should immediately report breaches in PPE such as a tear in gloves or any other potential exposures to their supervisor.

- Cleaning staff and others should clean hands often, including immediately after removing gloves and after contact with an ill person, by washing hands with soap and water for 20 seconds. If soap and water are not available and hands are not visibly dirty, an alcohol-based hand sanitizer that contains at least 60% alcohol may be used. However, if hands are visibly dirty, always wash hands with soap and water.

- Follow normal preventive actions while at work and home, including cleaning hands and avoiding touching eyes, nose, or mouth with unwashed hands.

- Additional key times to clean hands include:

- After blowing one’s nose, coughing, or sneezing

- After using the restroom

- Before eating or preparing food

- After contact with animals or pets

- Before and after providing routine care for another person who needs assistance such as a child

- Additional key times to clean hands include:

Additional Considerations for Employers:

- Employers should work with their local and state health departments to ensure appropriate local protocols and guidelines, such as updated/additional guidance for cleaning and disinfection, are followed, including for identification of new potential cases of COVID-19.

- Employers should educate staff and workers performing cleaning, laundry, and trash pick-up activities to recognize the symptoms of COVID-19 and provide instructions on what to do if they develop symptoms within 14 days after their last possible exposure to the virus. At a minimum, any staff should immediately notify their supervisor and the local health department if they develop symptoms of COVID-19. The health department will provide guidance on what actions need to be taken.

- Employers should develop policies for worker protection and provide training to all cleaning staff on site prior to providing cleaning tasks. Training should include when to use PPE, what PPE is necessary, how to properly don (put on), use, and doff (take off) PPE, and how to properly dispose of PPE.

- Employers must ensure workers are trained on the hazards of the cleaning chemicals used in the workplace in accordance with OSHA’s Hazard Communication standard (29 CFR 1910.1200).

- Employers must comply with OSHA’s standards on Bloodborne Pathogens (29 CFR 1910.1030), including proper disposal of regulated waste, and PPE (29 CFR 1910.132).

Additional Resources

The South Carolina hurricane guide contains helpful and practical tips for all chapters in the path of a hurricane. Check their website for the most updated version.

A hurricane is a storm with rotary circulation that originates in a tropical depression over the sea with winds in excess of 74 miles per hour. Hurricanes are usually accompanied by torrential rains and flooding along coastal areas. Hurricane season typically runs from June 1 to December 1.

The National Weather Service tracks tropical storms as they intensify into hurricanes. They issue advisories every six hours while a storm is more than 24 hours away from land and more frequently as it approaches landfall. The advisories state the storm’s location, wind velocity, speed and direction. The National Weather Service issues warnings when they determine that a coastal area will be affected by the storm’s high winds or a combination of high water and rough seas.

Every facility located in a coastal area should develop a hurricane emergency plan. The plan should include a detailed procedure and checklist for shutting down processes and protecting buildings, contents, equipment and yard storage. In addition, the procedures should include guidelines to follow to mitigate losses during the hurricane and salvage procedures to follow after the hurricane has subsided.

The plan should include the amount of time required (in hours or days) to complete each major task to ensure preparations are initiated at the appropriate time. Hurricane preparedness also should include the appointment of a qualified group of individuals to form a salvage squad. The objective of the salvage squad is to restore operations to normal as quickly as possible.

Preparation

Preparation for a hurricane should include both long-term and short-term plans.

Long-Term Preparation

Long-term plans should be established, completed and reviewed periodically. These plans will mainly encompass improvements to construction features and site preparation to minimize hurricane damage. Long-term preparations could require several weeks or months to complete.

Long-term planning should concentrate on installing and maintaining construction features to increase the “hurricane resistance” of the property. Any hurricane resistance feature that cannot be permanently installed should be arranged so that the specialized protection can be quickly and easily installed. Protection features will need to be inspected and tested at least annually (prior to hurricane season) to keep them in good repair. The following items should be included on the pre-hurricane checklist:

- Verify that roof-mounted signs and equipment, guy wires and supports are properly anchored and in good repair.

- Repair or replace any weak or damaged door hinges and latches.

- Verify auxiliary lighting is in working order.

- Complete all applicable items from Travelers Flood Protection, Preparation, Response and Recovery document.

- Establish a system to protect all windows and openings on the buildings.Installing shutters, bracing large doorways, having material available to cover all glass, etc., will complete this step.

- Establish an emergency response team and assemble necessary supplies and equipment at a central, secure location. Each year inspect and verify that the supplies are in good repair. Examples of supplies and equipment may include:

- Portable pumps and hose

- Mops and squeegees

- Emergency lighting

- Tarpaulins/plastic sheeting

- Lumber and nails

- Power and manual tools

- Sandbags

- Shovels and axes

- Building diagrams/schematics

- Ropes/fasteners

Any new construction or building remodeling should comply with the hurricane preparedness plan. Short-term plans should be developed well in advance of a hurricane, but need only be implemented when the projected path of a hurricane puts your facility in imminent danger of receiving damage. To prepare for an oncoming hurricane, detailed procedures and a checklist should be developed to ensure an orderly shut down of all production processes and all property is properly protected. The amount of time required (in hours or days) to complete each major task should be determined in advance to ensure preparations are initiated at the appropriate time..

Short-Term Preparation: As a Hurricane Approaches, Secure the Facility

As the hurricane approaches, quick action will need to be taken to install temporary protection features. The following actions should be completed:

- Shutter or board up windows to help protect them from flying debris.

- Clean out floor drains and catch basins. Check drainage pumps.

- Anchor structures, trailers and yard storage so they will less likely be moved by high winds. Move yard storage inside where practical.

- Anchor and fill above-ground tanks to capacity with product or water to minimize wind damage.

- Move drums and portable containers of flammable liquids to a secure properly protected area. Do not move these materials inside your facility unless you contact Travelers Risk Control to help determine if fire protection is adequate to allow inside storage of flammable liquids.

- Secure outdoor cranes in accordance with manufacturer’s instructions.

- Fill emergency generator and fire pump fuel tanks.

- Inspect all fire protection equipment to be sure it is in service.

- Move important records to a secure area that is protected from the elements. Duplicate critical records and move them offsite to a location that is not susceptible to the hurricane.

- Shut down production processes safely.

- Shut off all flammable liquid, combustible liquid and gas lines at their source to prevent an accidental release caused by broken piping.

- Complete all applicable items from the Flood section of Travelers Flood Protection, Preparation, Response and Recovery document.

- Shut off electrical power at the main building disconnect before the hurricane strikes.

- Evacuate all employees and, if safe for an emergency response team to remain in the building, ensure that the team has the following:

- Nonperishable food

- Suitable communication devices

- Stored drinking water

- Flashlights/batteries

- First-aid supplies

- Vehicles with full fuel tanks

- Dry clothing

- Boots/gloves/hard hats

Travelers Resources to Help You With Hurricane Preparedness

- Travelers Risk Control Prepare and Prevent

- Open for Business®, a Web-based, interactive disaster planning tool from the Insurance Institute for Business & Home Safety (IBHS).

Websites

- Ready.gov – Hurricanes

- NOAA – Hurricanes(Hurricane tracking, forecasts and alerts based on your zip code)

- Red Cross – Hurricane Preparedness

- Red Cross – Preparing Your Business (PDF overview of natural disaster preparedness)

During the Hurricane

Arrangements should be made to evacuate the emergency response team before the hurricane strikes. If the emergency response team is able to stay on site, a safe area of substantial construction should be available for the team members to occupy. The emergency response team plans should be communicated in advance to local law enforcement officials. The emergency response team should continually patrol the facility as long as it is safe to do so and complete the following:

- Watch for structural damage and make repairs as necessary.

- Watch for causes of fire (e.g., electrical short circuits, flammable materials floating on floodwaters, and flammable gas escaping from ruptured pipes) and take corrective action as needed.

- Check sprinkler water pressures frequently and watch for loss of pressure.

- Watch for flooding from rain or tidal surge and deploy sandbags as necessary.

After the Hurricane

Once the storm has subsided, the salvage squad should be assembled and the squad leader should assign job priorities to safely repair and restore production processes and buildings.

A properly staffed salvage squad generally consists of personnel who are qualified to repair electrical, mechanical, plumbing and fire protection systems. In addition, an adequate complement of personnel for general cleanup may be required. If outside contractors are used, they must be supervised to ensure safe operating conditions are maintained.

The squad leader should verify the salvage squad is properly staffed and equipped to complete their objectives. Typical supplies will include construction tools, mops, buckets, rust inhibitors, fans, water vacuums, brooms, dehumidifiers, squeegees, and wiping rags. Other non-typical items may include the need to order replacement motors, mechanical equipment, etc.

The salvage squad leader should verify the following items are completed

Immediate damage assessment should be completed and action plans developed to address priorities:

- Look for safety hazards such as downed power lines, exposed electrical wires, leaking gas, etc.

- Appraise buildings for structural damage or undermining of building foundations.

- Assess impaired fire protection equipment and alarms.

- Assess critical production equipment and valuable stock that is required to restore production.

- Complete temporary repairs and minimize hazards to ensure personnel can safely access the building.

The Salvage Squad Should

- Provide portable multi-purpose fire extinguishers

- Require strict precautionary measures for any cutting/welding that will occur in or around the buildings. Refer to Travelers document Cutting, Welding & Hot Work Operations for more information.

- Eliminate any unnecessary ignition sources and include the enforcement of “No Smoking” regulations.

- Establish a procedure for removing debris brought by the storm and as a result of any reconstruction efforts.

- Any holes or other penetrations in the building walls should be temporarily repaired.

- Assess and prioritize building contents that have been damaged and can be salvaged.

- Photograph and/or make a video recording of any building or content damage.

Fire Protection Equipment

- Assess and service fire pumps that were submerged. The pumps should be tested and placed back in service.

- Assess the integrity of fire protection alarm circuits. Fully test all alarms. Repair as needed.

- Assess the integrity of security alarm circuits. Fully test all alarms. Repair as needed.

- Physically test any sprinkler control valves that were submerged to verify they are operational. Conduct main drain tests for the sprinkler system(s).

- Notify the local fire department of any extended impairments that will be required for the above systems. It may be necessary to arrange for fire and security watch services for your building whenever protection is out of service.

Electrical Restoration Should Be Completed

- Do not energize electrical circuits in the buildings until an electrician has checked all systems.

- Care should be exercised around damaged power cables.

- The electrician should notify the squad leader and utility company of all necessary repairs.

- Electric motors, switch gear and cables should be thoroughly inspected, cleaned and dried as needed before energizing. Even if it has not been immersed, electrical equipment can absorb sufficient moisture to reduce its insulation resistance to a dangerously low level. While electrical leakage may be too small to blow fuses or trip the circuit breakers, it may be sufficient to cause overheating and fires.

- Carefully examine all metal-clad cable, lighting sockets, receptacles, snap switches or any devices with paper or fiber insulation.

Mechanical Equipment and Systems:

- Check all flammable liquid and gas piping systems and associated tanks for leaks or damage.

- Steam lines and any refractory-containing equipment should be examined for wet insulation. In some cases, if insulation is contaminated, it must be stripped and restored rather than dried in place.

- Test the water supply for boilers, process feed and cooling water, and test underground storage tank contents for contamination before use.

- Mechanical equipment should be cleaned and dried with casings opened for inspection. Shafting should be checked for alignment and lubricating systems flushed.

Security Service:

- Perform a continual fire watch until normal operations are resumed.

- Verify that personnel understand how to contact outside emergency response units.

- Provide suitable communication equipment so personnel can immediately contact emergency response units.

Familiarize personnel with any unsafe or hazardous conditions and update them with the progress of salvage operations.

The information provided in this document is intended for use as a guideline and is not intended as, nor does it constitute, legal or professional advice. Travelers does not warrant that adherence to, or compliance with, any recommendations, best practices, checklists, or guidelines will result in a particular outcome. In no event will Travelers, or any of its subsidiaries or affiliates, be liable in tort or in contract to anyone who has access to or uses this information for any purpose. Travelers does not warrant that the information in this document constitutes a complete and finite list of each and every item or procedure related to the topics or issues referenced herein. Furthermore, federal, state, provincial, municipal or local laws, regulations, standards or codes, as is applicable, may change from time to time and the user should always refer to the most current requirements. This material does not amend, or otherwise affect, the provisions or coverages of any insurance policy or bond issued by Travelers, nor is it a representation that coverage does or does not exist for any particular claim or loss under any such policy or bond. Coverage depends on the facts and circumstances involved in the claim or loss, all applicable policy or bond provisions, and any applicable law.

Contrary to public perception, earthquake preparedness is not just an issue in California. This resource from Travelers, the insurance company for MJ Sorority clients, offers tips to help protect your business before, during and after an earthquake.

Get information on preparing for natural disasters such as earthquakes, floods, tornados, hurricanes, wildfires, etc. This resource from Travelers, the insurance company for MJ Sorority clients, discusses exposure assessment, protection, planning and preparation, response, and recovery.

A resource developed for universities from Travelers, the insurance company for MJ Sorority clients, much of which is applicable to sororities as well.