A practical framework for prevention, early detection, and summer shutdown management

Mold is one of the most preventable property issues facing sorority chapter houses. While unaddressed roof leaks and plumbing failures can certainly be a catalyst for mold growth, hidden moisture inside HVAC systems and ductwork can quietly create conditions for mold growth long before visible damage appears. Summer presents a particularly heightened risk with higher temperatures and empty chapter houses. When houses sit vacant, occupancy-driven air circulation drops, thermostats are adjusted and deferred maintenance can allow humidity to build unchecked.

For sorority housing, mold that grows over the summer months can cause chaos at the start of the fall semester. Discovering mold shortly before move-in or at move-in can delay occupancy and lead to costly remediation.

Why HVAC Systems Are Often the Culprit

HVAC systems are frequently the hidden source of mold problems because they naturally produce condensation and move air throughout the building.

Common causes include:

- Poor humidity control (indoor humidity consistently above 60%)

- Dirty evaporator coils, where dust + moisture create organic growth surfaces

- Improperly insulated ductwork, leading to condensation on vents and ducts

- Systems cycling too infrequently in vacant summer months, allowing stale, damp air to linger

- Negative pressure issues, pulling humid outside air into the structure through gaps and cracks

Once mold develops in HVAC components, spores can be distributed throughout the property, rapidly expanding the areas impacted.

Early Warning Signs

The earlier mold is caught, the easier it is to address. House corporations and property managers should walk properties weekly and look for:

- Persistent “musty” or earthy odors

- Condensation and/or dark spotting on vents, windows, or supply registers

- Damp or clammy indoor air (60% + humidity)

- Unexplained staining on ceilings or walls

- Warped trim, bubbling paint, or peeling wallpaper

- Rust or standing water in drain pans

- Visible buildup on coils or inside air handlers

- Increased HVAC runtime with poor dehumidification

- Blocked condensate lines

Best Practices for Summer Mold Prevention

The strongest mold strategy is proactive building management:

- Maintain indoor relative humidity between 45–55%

- Avoid shutting HVAC systems off completely during summer vacancy and program systems for consistent cycling

- Install standalone commercial dehumidification where needed

- Use remote humidity and temperature monitoring sensors with alerts

- Thoroughly inspect and clean drain pans and drain lines before vacancy

- Replace filters on schedule

- Clean coils annually

- Verify ducts are sealed and insulated properly

Weekly summer walkthroughs should include checking for warning signs, particularly in:

- Mechanical rooms

- Basements

- Utility closets

- Behind furniture near exterior walls

- Attics and roof penetrations

- Bathrooms and kitchens

- Supply/return vents and duct chases

A Smart Chapter House Approach

The best-managed houses treat mold prevention as part of a broader, proactive property management strategy, rather than reactive maintenance. Monitoring humidity, maintaining HVAC systems, and conducting summer inspections are relatively modest investments to prevent highly disruptive and costly remediations to your property.

A dry building is a resilient building. Continue to be wary of mold during the summer months and ensure that air flow and property inspections are a part of your chapter’s summer operations.

Sorority housing is a shared environment and the way members and staff use the property directly impacts the safety, functionality, and long-term resiliency of the chapter house.

One of the most common and most preventable sources of property damages in chapter house facilities is improper use of plumbing systems. What goes down the drain does not magically disappear! Over time, certain materials accumulate within pipes, increasing the likelihood of blockages, backups, and costly repair.

We have partnered with Fluid Waste Services to compile a list of the most frequent offenders of sewage blockage and backups and the best practices to combat pipe and resulting property damage. This guidance is intended to support responsible use of plumbing systems and to outline best daily practices, as well as proactive maintenance strategies to protect your chapter house.

Toilets: What to Flush

Toilets are designed to handle human waste and toilet paper. That’s it! Pretty simple, right? Wrong. Chapter members often flush feminine hygiene products, wipes (including those labeled “flushable”), hair, floss, cotton swabs, and more. Posting clear and visible signage in your bathroom facilities outlining what’s “flushable” can help combat this problem. Our team has created a flyer included in this article for your use.

It’s also prudent to keep in mind that vomit is highly acidic and can, over time, contribute to pipe deterioration. When possible, it’s always best to use a trash can when fighting a stomach bug.

Showers & Sinks: Protecting Your Drain

Hair, along with wipes, are the most common causes of bathroom clogs. To reduce the risk of clogs:

- Do not allow hair, wipes, cotton products, dental floss, bandages, or contact lenses to enter drains;

- Use hair catchers in showers; and

- Instruct members to dispose of all personal care items in the trash.

Be sure that your cleaning vendor or other responsible staff member is well versed in this risk management technique. Drains should be inspected and cleaned regularly and women living in the chapter house reminded to refrain from putting any of the materials listed above down any drain.

If a pipe or drain becomes clogged and begins to backup, leak detection technology can be helpful in identifying water before it becomes a larger problem. Click here to learn more about these systems and their advantages.

Kitchen Sinks: Grease and Food Waste

Bathrooms aren’t the only common place where pipes get backed up. Kitchen drains are also particularly vulnerable to buildup and blockage.

Grease, including oil, butter, fats, and sauces, is one of the leading causes of sewer issues in shared housing. When poured down the drain, grease cools and solidifies within pipes, restricting flow and increasing the likelihood of backups.

The following should never go down the kitchen drain:

- Grease, oil, butter, or fats;

- Food scraps (including rice, pasta, and coffee grounds);

- Egg shells; or

- Flour or dough

This applies even when a garbage disposal is present.

Best practice is always to allow grease to cool, transfer it to a container, and dispose of it in the trash. Chefs, kitchen staff, and members should scrape all plates and cookware into the trash before washing. Kitchen staff handling grease should be sure that it’s handled with care and completely cooled before throwing in the trash as it can become a fire hazard.

Proper food disposal can also be encouraged by strategically placed signage in dining and kitchen areas. This is especially important for open kitchens, where women are presumably using the kitchen without supervision.

Proactive Maintenance

In addition to the daily best practices outlined above, proactive maintenance of your entire plumbing system is essential. High frequency of use places significant strain on pipes, making routine inspection and cleaning a key component of preventing plumbing failure.

At a minimum, the following maintenance standards should be observed:

- Annual professional inspection: Camera inspection of the main sewer line to identify early-stage blockages, regular pipe deterioration, or root intrusion.

- Preventative cleaning: Performed 1-2 times annually (depending on usage and claims history), with emphasis on kitchen lines and bathroom drains to unclog potential blockages

- Trigger-based inspections: Evaluations should be performed immediately if any warning signs appear including slow drains, recurring clogs, odors, or gurgling pipes

These best practices allow for issues to be uncovered before they become larger problems and extend the life of your plumbing infrastructure.

Why This Matters

These may seem like small suggestions, but they make a big difference in the health and maintenance of your pipes. While damage can sometimes be immediately apparent, often less obvious ware and tear of pipes is accelerated and the consequences heightened by everyday practices by those that use the plumbing.

Improper drain use is not a minor inconvenience and the consequences of improper use and maintenance can interrupt member experience, cause secondary perils like mold or other biohazards, and lead to even larger problems down the road. From a financial standpoint, these events can be significant. Clearing a single blockage may cost several thousand dollars, while pipe repairs or replacement can escalate to five to ten times that amount.

If you have any concern about the health of your pipes or want to better understand the types of materials and other conditions of your plumbing systems, it’s recommended to contact a plumbing company who can scope your plumbing infrastructure and offer as assessment of its health.

Conclusion

Maintaining the health of your plumbing infrastructure ultimately comes down to consistency in daily practices and preventative maintenance. Post clear signage (we created some signage for your use), ensure that annual maintenance visits are planned and executed, and educate your members, staff, and vendors on signs of blockage or other pipe damage.

When these principles are embedded into operations and culture, your property is better positioned to operate smoothly with fewer unexpected disruptions over time.

At this year’s MJ Housing Forum, we shared our communications calendar to help chapters and house corporations stay ahead of emerging risks. This quarterly graphic highlights the key topics, reminders, and resources we’ll be focusing on throughout the year—so you know what’s coming, when it matters, and how to prepare. We thought it might be helpful to share here as well.

Winter can be especially hard on chapter facility roofs — even when there are no obvious signs of trouble. Snow load, ice dams, freeze-thaw cycles, high winds, and fluctuating temperatures all stress roofing systems in ways that may not be visible at the time. In many cases, damage that begins in January does not reveal itself until March or April — when melting snow and spring rains find pathways into the building.

As we move toward warmer weather, now is the right time to revisit the fundamentals of roof management and inspection.

Why Winter Damage Often Appears in Spring

Several common winter conditions contribute to delayed roof issues:

Freeze–Thaw Cycles

Water can enter small cracks or seams in roofing materials. When temperatures drop, that moisture freezes and expands, widening gaps and weakening seals. Repeated cycles can compromise flashing, membranes, and shingles.

Ice Dams

Ice dams form when snow melts and refreezes at roof edges. Water trapped behind the ice can back up under shingles and flashing, leading to interior leaks that may not appear until temperatures rise.

Snow Load & Structural Stress

Heavy snow adds weight to the roof system. Even if structural damage is not visible, prolonged load can strain decking and fasteners.

Wind Damage

Winter storms can loosen flashing, lift shingles, or damage roof penetrations. The impact may not be apparent until water intrusion begins.

Warning Signs to Watch For This Spring

As snow melts and spring rains begin, house corporations and facility volunteers should be alert for:

- Water stains on ceilings or walls – even minor staining can indicate a larger issue developing above

- Peeling paint or bubbling drywall

- Musty odors in upper floors or attic spaces

- Dripping near chimneys, vents, or skylights

- Shingles or roofing materials visible on the ground

- Damaged or detached flashing

- Flashing is thin metal installed at roof joints and transitions — most commonly around chimneys, vents, skylights, roof-to-wall intersections, and valleys — to direct water away from seams and prevent leaks.

Proactive Roof Management: Best Practices

Effective roof stewardship is not reactive — it is scheduled and documented.

1. Schedule a Professional Inspection

Early spring is an ideal time for a qualified roofing contractor to inspect the system, especially after a harsh winter. A documented inspection helps identify small issues before they become significant claims.

2. Maintain Clear Drainage

Ensure gutters and downspouts are clear of debris. Poor drainage accelerates roof deterioration and increases the risk of ice dam formation.

3. Document Repairs and Maintenance

Keep organized records of inspections, repairs, and warranties. Documentation supports long-term capital planning and can be important if a claim arises.

4. Plan for Replacement — Don’t Delay It

Roofs have a finite lifespan. If your system is nearing the end of its useful life, proactive replacement is typically far less disruptive and less costly than emergency repairs following a failure.

5. Address Small Leaks Immediately

Water intrusion rarely improves on its own. Prompt attention limits interior damage, mold development, and secondary costs.

Insurance Considerations

While insurance policies may respond to sudden and accidental damage, they are not intended to cover wear, tear, or deferred maintenance.

A well-maintained roof not only protects members and property — it also supports favorable insurance outcomes and reduces the likelihood of large, avoidable claims.

A Seasonal Reminder

Spring is a natural checkpoint for facility review. As part of your broader risk management efforts, add roof inspection and maintenance to your seasonal planning calendar.

If you have questions about roof management, capital planning, or property risk mitigation, MJ Sorority is here to help.

Across the U.S., disaster-related losses have exceeded $1 trillion in just the past seven years—but it’s not only hurricanes or wildfires causing damage. More frequent threats like water leaks, power outages, and storm damage are becoming costly realities. For house corporation volunteers, the old approach—“buy insurance and react to loss”—is no longer sufficient. With insurers tightening terms and raising premiums, proactive risk hardening is now essential.

What Is “Risk Hardening?”

Risk hardening means taking proactive steps to make your chapter house stronger, safer, and better prepared to handle damage from things like storms, water leaks, or power outages.

It’s about investing in simple upgrades, preventive maintenance, and smart planning to reduce the chances of serious damage—and to help your facility bounce back quickly if something does go wrong.

For example, installing leak detection sensors, reinforcing the roof, trimming back trees, or creating a basic emergency plan are all ways to “harden” your risk.

Think of it as safeguarding the chapter house now to avoid bigger problems later.

Why You Should Care

Taking preventive steps can significantly reduce both financial and operational impact for chapter houses. Every $1 spent on mitigation saves roughly $4–6 in post-disaster recovery costs. That’s savings you can invest back into your facility and protect your members’ well-being.

Smart Risk Hardening Measures

| Area | What to Do | Resource |

|---|---|---|

| Leak Detection | Install flow-based leak protection systems and strategically place water sensors under appliances and pipes. | Learn more about leak protection systems, including how to qualify for a premium credit: Leak Protection |

| Flood & Sewer Backup Prevention | Use sump pumps, direct water away from the foundation, and consider sewer-backup prevention devices. | See Preventing Water Damage |

| Roof Hardening & Storm Preparation | Reinforce roofs with impact-resistant materials and clean gutters and downspouts to improve water flow. | Learn more about maintaining your roof. |

| Security Enhancements | Improve exterior lighting, secure locks, clear sightlines, and use biometrics or smart cameras. | Watch Smart Security Strategies for Chapter Houses webinar. |

| Self-Inspection & Preventive Maintenance | Complete MJ Sorority’s Chapter House Self-Inspection form at least annually—summer is an ideal time. | Download MJ’s Chapter House Self-Inspection Form. |

| Emergency Readiness | Prepare an emergency response plan and keep updated inventories and documentation of property and valuables. | Review emergency resources at MJ Sorority. |

Beyond Bricks and Mortar

Risk hardening isn’t just about upgraded building materials—it’s about thoughtful planning and clear communication:

- Emergency Response Plan: Train volunteers and collegiate leaders on evacuation, communication, and critical contacts. This resource can help.

- Documentation Management: Keep photos, floor plans, insurance records, and inventory lists backed up securely. Check out our House Corporation Inventory Checklist to help.

- Regular Walkthroughs: Use the self-inspection form and monthly to-do lists to spot small issues before they grow.

The Bottom Line for House Corporation Volunteers

Being proactive is more than a best practice—it’s a duty of care. Your role is to steward the property for current and future members. Strengthening the chapter house today not only limits financial loss—it fosters a safer, more secure environment for your members and your organization.

As always, contact us with any questions.

Summer often brings quieter campuses—but it also brings an uptick in severe weather risks. From torrential rain and flash flooding to high winds, hurricanes, and even tornadoes, the summer season can cause serious property damage, particularly when chapter houses are unoccupied or unmonitored.

While you can’t prevent storms, you can reduce their impact by preparing the facility in advance. Here are five smart steps house corporations and property managers can take now to protect the chapter house during the summer months.

1. Identify and Address Hidden Vulnerabilities

Storm damage is often worsened by small maintenance issues that have gone unnoticed. Roof leaks, cracked foundations, blocked drainage, or worn seals around doors and windows can all become big problems when severe weather hits.

Before the height of summer storm season, walk the property or coordinate a professional inspection. Focus on known weak spots—roof seams, basement entries, foundation cracks, and aging drainage systems. Clear gutters and downspouts to ensure water flows away from the house, not toward it. Fixing these issues now can help avoid emergency repairs and insurance claims later.

Applicable MJ resources to help:

2. Establish a Local Emergency Contact

With the chapter members away during the summer, having someone nearby who can respond quickly is essential. Designate a local point of contact—such as a House Director, House Corporation volunteer, chapter advisor, or trusted contractor—who can monitor severe weather alerts and physically check the house following a storm.

This person can assess damage early, prevent additional losses (such as water intrusion), and coordinate immediate repairs. Even something as simple as tarping a roof or boarding a window can make a major difference in preventing further damage.

Applicable MJ resources:

3. Don’t Underestimate Flood Risk

Flooding isn’t just a coastal or river-adjacent risk—it can happen anywhere, especially when sudden storms overwhelm local drainage systems. Older homes or those with basements are particularly vulnerable.

Evaluate your property’s risk and consider steps such as:

- Sealing basement walls and windows.

- Installing or testing sump pumps, ideally with battery backups.

- Relocating key items—like mechanical systems or stored furnishings—above ground level.

- Maintaining relationships with local contractors and remediation vendors so help is readily available if needed.

Read more about increasingly severe storms and how best to prepare. Learn more about leak detection technology to help minimize water damage.

4. Prepare for Wind Damage Before It Happens

High winds from summer storms can be incredibly destructive. They can tear off shingles, topple trees, and turn outdoor furniture into airborne hazards.

Help reduce your risk by:

- Inspecting and repairing roofing and flashing.

- Trimming tree limbs that hang over the building or utility lines.

- Securing or storing outdoor furniture, signage, or trash bins.

- Reinforcing vulnerable exterior elements, such as entry doors or older windows, especially if the house is located in a hurricane or tornado-prone area.

Applicable MJ resources to learn more:

5. Emergency Planning Isn’t Optional—It’s Essential

Having a documented emergency response plan is a crucial part of risk management, but a plan that’s never shared or practiced won’t be much help in the middle of a storm. House Corporations should take time each year to review and update their storm and emergency procedures. Make sure everyone involved—house directors, local volunteers, advisors, and key vendors—knows their role before a crisis occurs.

Think through the key questions:

- Who monitors local weather alerts and determines when action is needed?

- Who checks the property after a storm or initiates emergency repairs?

- What’s the communication plan between the House Corporation, volunteers, and headquarters?

- Do all relevant parties have access to important documents, contact lists, MJ claims contact, and vendor information if power or internet is down?

Even if the house is unoccupied, a clear response protocol helps minimize damage, speeds up repairs, and keeps everyone informed and prepared.Bottom of Form

Advance Planning Makes a Big Difference

With the chapter house unoccupied, it’s easy for minor issues to go unnoticed until they become major problems. Taking time now to prepare for summer weather can protect the property and reduce your to-do list come fall move-in. If you’re unsure where to start, your MJ Sorority team is always here to support you.

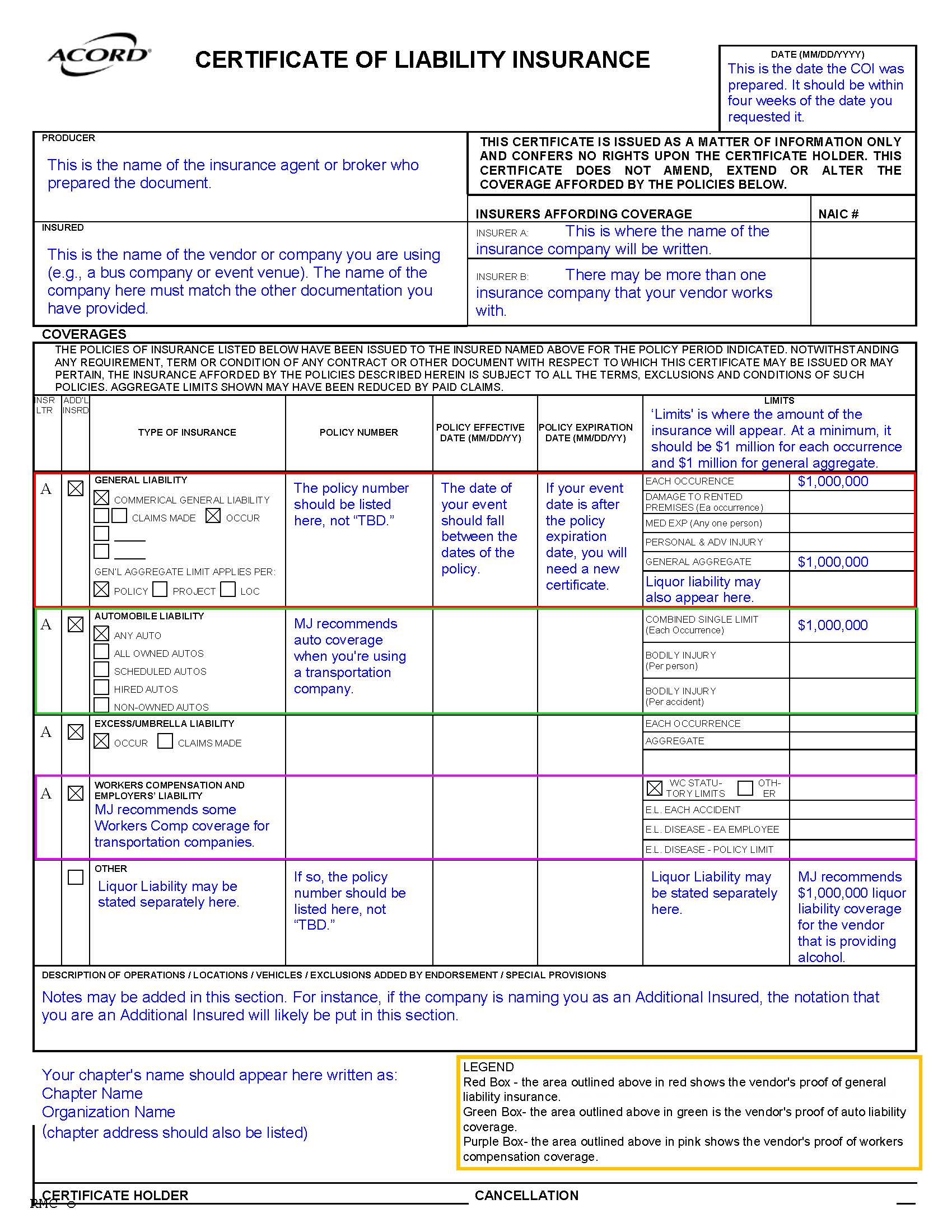

When you’re hosting an event at a venue or other third-party location, your organization’s guidelines require that you obtain proof of insurance from that venue. This is done through a certificate of insurance. A certificate of insurance (COI) is a document that shows a business has insurance coverage. The venue may very well also request to see your organization’s COI, which you can request here (remember you need to have a written request from the venue, often found in your contract!). And be sure to obtain a venue’s COI before signing a contract with the venue for your event.

A certificate of insurance is an official document that summarizes an organization’s insurance coverage. It is the only acceptable form of this confirmation and is part of your due diligence in vetting the venue for an event. Sometimes venues offer declarations sheets or other parts of their policy as proof of insurance. This is not the same as a certificate and should not be accepted.

So you’ve gotten a venue’s certificate of insurance—now what? Certificates of insurance include a wide variety of information, some of which is important, and some of which isn’t relevant to your review. When you receive a certificate, the following are items you should absolutely look for:

Who is the named insured? The named insured should be the name of the vendor. Sometimes this may be a different name “doing business as” the “name of the venue”. For example, if you’re hosting an event at ABC Event Center, the venue’s COI may have the named insured listed as “XYZ Corporation, doing business as ABC Event Center”.

What are the policy limits? MJ recommends that third parties hold the following minimum limits of liability insurance:

| General Liability ($1,000,000 per occurrence) | Liquor Liability ($1,000000 per occurrence) | Automobile Liability ($1,000,000 per occurrence) | Workers’ Compensation ($500,000 per accident) |

| Any third party contractor should hold this amount of general liability coverage | This is recommended if the third party vendor is serving alcohol at a chapter event | This is recommended for third parties providing transportation, such as a bus company | We recommend this coverage for any contractors you engage with |

If a third-party does not hold these minimum limits, please contact your headquarters to determine whether you need to identify an alternative option. There may be some exceptions and differentiations in your organization’s event guidelines.

Liquor liability in particular can be tricky as sometimes it’s listed separately and sometimes is included in the general liability coverage. If it’s included under the general liability section, liquor liability coverage will be noted specifically and you should be able to easily deduce that there is adequate coverage.

What are the policy effective dates? The effective dates are typically one year in length and should cover the date(s) of your event. If the policy is for a short period of time or do not cover the date(s) of your event, the certificate does not provide proof of coverage for your event and you should reach back out to the venue to get clarification and another certificate that provides proof of adequate coverage for your event.

Is your organization listed as a certificate holder? Being a certificate holder means you’re receiving a (COI) to verify that the policyholder has adequate insurance coverage. You are not covered by the policy and don’t have any rights under it. While this may not be required by your organization, it confirms that you have received an up-to-date policy pulled specifically at your request.

Most certificates are relatively straightforward, however, there are some things to look out for that may be problematic:

- Be sure text hasn’t been superimposed on an existing certificate. This is fraudulent and should not be accepted.

- Be sure that the certificate is complete and matches the information in your contract with the venue (i.e. address, name, etc.)

- DO NOT accept COIs that list effective dates as covering one day or a very short period of time. These policies are not acceptable and will not provide adequate coverage in the event of a claim and typically exclude sororities. If you have questions about a policy term, please contact your headquarters

Obtaining a COI is a vital risk management practice when planning events and is a lifelong skill! When hiring a contractor to work on your home or hosting a wedding or baby shower for a friend, you will again run into certificate review.

Click here for a sample COI with our recommendations.

Officer transitions are a pivotal time for any sorority chapter. A well-executed transition maintains stability and preserves institutional knowledge. Without proper planning, chapters risk losing valuable experience and insight. We are noticing how important it is for chapter officers and advisors to help train their replacements to ensure continuity, especially in the area of event planning.

No matter what time of year your officers are transitioning, here are some tips to make officer transitions seamless and effective:

1. Start Early

Transitions shouldn’t begin when new officers are elected—they should be an ongoing process. Encourage outgoing officers to document their roles and responsibilities throughout their term so new leaders don’t have to start from scratch.

2. Create a Comprehensive Officer Manual

Each position should have a detailed manual outlining key duties, deadlines, and best practices. This can include:

- Contact lists for campus administrators, advisors, and other key contacts

- Budget templates and financial records

- Event planning timelines and risk management protocols

- Past successes and lessons learned

- Important websites and resources

- Be sure to check with your national headquarters for officer manual templates

3. Hold One-on-One Training Sessions

Outgoing officers should meet individually with their successors to provide hands-on training. Walking through daily tasks, software tools, and decision-making processes helps new officers feel more prepared. We are also available to develop and deliver risk management education for officers during larger officer transition periods. Contact Kit Moorman, Director of Risk Management Education, for more information.

4. Conduct a Full Executive Board Transition Meeting

A group meeting with both outgoing and incoming executive boards fosters collaboration and alignment on chapter goals. This is also a great time to discuss upcoming initiatives, potential challenges, and strategic plans for the year ahead.

5. Leverage Mentorship from Alumnae and Advisors

Advisors and alumnae can provide continuity by offering historical context and best practices. Encourage new officers to maintain open communication with these key resources.

6. Utilize Digital Storage for Important Documents

A shared, organized digital archive (such as Google Drive or a chapter management platform) ensures critical documents are easily accessible and not lost between transitions.

7. Encourage Reflection and Feedback

Ask outgoing officers to share what worked well and what could be improved. Creating an open dialogue allows new leaders to learn from past experiences and refine their approach.

By prioritizing a structured transition process, chapters can ensure their new officers step into their roles with confidence, armed with the knowledge and resources they need to succeed. A strong transition plan not only preserves the chapter’s legacy but also sets the foundation for future success.

Even with protections put in place by internal IT departments or outside partners, email remains an unsecured and unreliable technology capable of being hacked, altered and manipulated. Read this report by our partners at CHUBB outlining some of the most prominent tactics that bad actors are using in their social engineering schemes. Included are examples of the most common schemes and the best ways to prevent them.

In an ideal world, house corporations can evaluate the physical state of their properties and plan to address concerns and make updates to chapter houses as their schedules and financial circumstances allow. However, in the real world, this isn’t always possible and work needs to be done on the property due to unforeseen weather damage, a water leak, or other unexpected event that can lead to a claim.

Roof damage can be particularly disruptive and requires immediate attention. As your partner in managing these claims, MJ wants to be sure you’re thinking about the long-term implications of the choices you make when repairing or replacing the damaged roof. As always, our goal is to carry the claim effectively and efficiently through the process with your carrier and make you aware of the latest technologies and materials to consider when addressing the damage to your property.

As you begin repairs and/or replacement of your roof, we would encourage you to consider, at the very least, an assessment of the state of your roof before beginning repairs. This is best practice when beginning repairs on any claim as you consider the efficiencies and potential benefits of making improvements along with repairs.

Your current carrier provides comprehensive coverage to “repair or replace the damaged area with materials of like kind and quality.” Addressing your roof claim is the perfect opportunity to implement additional fortification measures that may prevent or mitigate future damage. Most notably, while you may receive quotes that meet your state’s building code requirements, these should be treated as the minimum of repairs, and you should strongly consider hiring a contractor that will take additional measures to fortify your roof with technologies like impact resistant shingles and wind and rain resistant ventilation. An impact resistant shingle may run 15%-20% more than the cost of a composite shingle, but will save you in the long run, withstanding higher winds and more effectively keeping water out of the house. While these decisions may be difficult to make when you’re making improvements beyond the replacement value covered by your policy, we firmly believe that the use of higher quality materials will save you in the long run.

You are likely going to be replacing shingles that, due to their age, are not engineered to be as wind resistant as the newer, more advanced shingles available on the market today. Worsening weather conditions have included significantly stronger winds in areas that have not historically experienced such extreme weather, waring on older structures not built to withstand increasingly high winds. This map, maintained by FEMA, may help you evaluate your risk for wind at your property. You will need to evaluate whether the increased cost of these shingles and other fortification measures will save you in the long run should another wind/hail incident occur. Also consider a 6-nail installation of shingles to help fortify your roof.

See below for resources outlining these innovative solutions, measures we believe are imperative to maintaining your insurance coverage long term and maximizing the longevity of your roof. Also included is a webinar with contact information for our business partner, Bone Dry, who may be able to provide an assessment of your roof and provide recommendations for fortification.

Out of Sight, Out of Mind: The Importance of Roof Inspections

Updating and Maintaining Your Chapter House Roof

Webinar: Managing Your Chapter Roofs with Bone Dry

If you are able, a claim can be an opportunity to make improvements to your chapter house roof and prevent future damage. Reducing the frequency and severity of future claims to your roof serves to maintain your premium and preserve the comprehensive coverage that the MJ Sorority program provides. We encourage you to reach out to our team with any questions about preferred materials as you make a plan to repair or replace your roof.

As a property owner of a sorority chapter house, you likely keep a close eye on the building’s interior, exterior, and overall maintenance to ensure it remains safe and well-kept. However, there’s one critical area that might not get the same level of attention — the roof. Since it’s “out of sight,” it often becomes “out of mind.” Unless there’s visible interior leaking or a recent windstorm, roofs rarely make it onto a regular inspection or maintenance plan.

Why This Matters Now

If you’ve been keeping up with MJ Sorority’s newsletters over the past two years, you know the property insurance market is experiencing significant challenges. Insurance companies are grappling with rising property claims due to changing weather patterns, which has led to several adjustments, including:

- Increasing property rates and premiums

- Raising standard deductibles for all causes of loss

- Implementing higher deductibles for specific risks like wind, hail, and water damage

- Adding stricter coverage limitations for roof damage

- In some cases, withdrawing from certain markets entirely, such as homeowners insurance in Florida and California

Fortunately, the insurance company providing sorority property coverage has taken a more balanced approach to these market shifts. However, to maintain comprehensive coverage, proactive risk management — like roof maintenance — is key.

The Value of Annual Roof Inspections

We’ve consulted with roofing contractors, and the message is clear: regular roof inspections are essential. Here’s why:

- Early Problem Detection: Routine inspections catch small issues before they turn into major (and costly) problems, helping to prevent damage to the structure.

- Extended Roof Lifespan: Addressing minor repairs early helps prolong the life of your roof, protecting both the building and your financial investment.

- Budget Planning: Insurance companies are increasingly concerned about property owners not accounting for the lifespan of roofing materials. Proactive inspections help you plan and budget for the inevitable roof replacement, rather than being caught off guard.

Getting Started

Travelers Insurance offers a helpful resource to guide your roof inspection planning: How to Build a Commercial Roof Inspection Plan.

The frequency of roof inspections will depend on various factors, so we recommend consulting with a qualified roofing contractor to determine the best schedule for your chapter house. As insurers continue to scrutinize roof conditions, incorporating regular inspections into your property maintenance program is more important than ever.

By taking these proactive steps, you not only help protect your chapter house but also contribute to maintaining stable and comprehensive insurance coverage for the sorority community.

ACH transactions are electronic money transfers made between banks and credit unions across the Automated Clearing House (ACH) network. While convenient and sometimes appropriate, you should NEVER fulfill a request to wire money from an email alone. Below are some examples of language vetted by a cyber law firm that can be helpful to include in your email signature as notice of your organization’s best cyber practices on this topic:

- [CLIENT] will never send an email requesting that wiring, ACH, or other payment instructions be changed or altered. if you receive a similar request from anyone, you should always confirm billing or payment instructions with a known contact in person or, if not possible, over the phone, so that you can confirm the identity of the sender. If you ever receive or have received a request from [client] regarding payment instructions via email only, please reach out to a known contact at [CLIENT] in person or by phone. Always contact our main number and do not utilize the phone number in the email you receive.

- Never wire transfer money based on an email request from our office without calling this office and speaking with someone personally to confirm wire information. When calling, do not use the phone number from the e-mail signature line. Even if an email looks like it has come from this office, or someone involved in your transaction, do not accept emailed wire instructions from anyone without voice verification. You will never be instructed to wire money related to a payment without verbal consent.